Programmable Money, Unprogrammable Continent

Yet another Money 20/20 Europe 2026 recap.

Hello there,

Last year I closed my Money 20/20 piece with a small prayer: that this year the floor would stop talking about stablecoins and AI in the abstract, and start talking about agentic commerce and MCP servers. A year later, it seems my closing wish was partly true.

Money 20/20 Europe turned ten in Amsterdam this June, and the official themes were AI and the Agentic Age, The Great Rebundling, Money Stack Rewired, and Regulation in the Fast Lane. Translation: agents, stablecoins, real-world use cases, and the plumbing underneath both.

Before this turns into yet another stablecoin recap of the event, here are a few headlines that were announced on the floor over the three days:

🇬🇧 The UK Payments Initiative (UKPI) launched with 31 banks and fintechs backing a commercial Variable Recurring Payments (VRP) scheme aimed at dislodging the card duopoly. The newest UK scheme since Faster Payments in 2008. - Read more about VRP here

🤖 Worldline, ING and Mastercard completed what they call the first live, end-to-end agentic payment in production. An agent found anniversary concert tickets, stayed within budget, and paid after approval.

🪙 Moneygram launched MGUSD, a dollar-native stablecoin (with Bridge/Stripe, M0, Stellar and Fireblocks), and announced it’s rebuilding the whole company on-chain.

🇪🇺 EPI/Wero showed working cross-border interoperability across multiple local payment schemes: Bizum🇪🇸, SIBS(MB WAY)🇵🇹, Vipps MobilePay🇳🇴 and BANCOMAT🇮🇹. A real pan-European A2A alternative is starting to take shape.

🇬🇧 GOV.UK picked Adyen over Stripe to power payments for its over 1,000 public-sector services, with pay by bank baked into the mandate.

🏛️ LSEG launched Identity Gateway, a single access layer into multiple national, private, agentic(?) identity schemes.

📈 OpenPayd filed to go public via SPAC in a merger with Titan Acquisition Corp valuing it at ~$1.145bn, listing on Nasdaq as “OP.”

Now, the themes.

Stablecoins

As the saying goes, “there is nothing new under the sun”, and stablecoins are still a largely misunderstood piece of technology, which is not helped by the insistence of providers in selling it like a product alternative rather than an enabling technology.

With over 40 panels on stablecoins, the messaging on this technology is yet to be coherent for outsiders.

While infrastructure providers are already live, enabling legacy businesses to integrate stablecoins and earn revenue. Others are still building MVPs that add complexity for the end user rather than abstracting it away. At the same time, banks and providers repeatedly asked for end customer use cases beyond institutional, custody, clearing, settlement, and treasury.

A few folks asked during panels: SEPA just works, and we have seen what Wero hopes to achieve with cross-border, so why do I need to download a stablecoins app?

In his panel with Dima Kats of Clear Junction, Olugbenga Agboola of Flutterwave said: "My mother in Canada knows about the Send App. She does not know about or need to know about stablecoins, GhIPSS or NIBSS. All she knows is that she opens the app, and the money is deposited in the account of her church in seconds. Send was doing this for her without stablecoins and will continue to do so with stablecoins where possible.”

“Stablecoins are not a product, but a faster settlement layer sitting on top of the payout network Flutterwave already runs. Money now moves at the speed of the internet rather than the speed of banks closing for the day, presenting a treasury-and-FX use case that especially works for us as African banking hours and correspondent rails don’t overlap.” - Olugbenga Agboola

Stablecoins scaling will be because of proper local distribution and the compliance depth to turn it into spendable money in each market, and not because everyone mints their own token. Stablecoins don’t make the intermediary obsolete; they complement the job of the various intermediaries that exist today.

Thanks to Arthur Bedel, I also had an opportunity to explain the famed Stablecoin Sandwich and the African context—how difficult it is to build a remittance or off-ramp solution for 54 countries—to the folks at DFNS.

Closing thought on this topic: what will make a shopper in Amsterdam pay for Nike trainers in stablecoins instead of a card, iDEAL or Klarna? As of now? Nothing. The live use cases still sit in cross-border, treasury and settlement, and almost all of it is still USDT and USDC. This is a piece of technology that is most useful for institutions yet keeps being presented as consumer technology. Repeating that it’s faster, cheaper and better ad nauseam will not change that fact.

*Agentic Commerce

Agentic commerce was the topic I most wanted to see more of this year, and the people who spoke on it did not disappoint. The clearest framing I heard was that agentic commerce needs four standard levels of autonomy to scale: discovery, assisted checkout, delegated action, and agent-to-agent commerce on a human mandate.

Another point I heard: product catalogues on the traditional rails used to carry 10-12 fields, and agentic commerce needs 30-40 or more. Rewriting catalogues at that scale is where the real work needed to scale this technology to mainstream usage is.

Just like stablecoins, the easiest machine-to-machine use cases to solve with today’s technology are the B2B ones. An agent can already pay for the compute and API credits it consumes on its own. But the integration starts to break at the marketplace when I tell an agent to buy a pair of pink Nike sneakers in size 14.

There’s still infrastructure to put in place, such as merchants of record, chargebacks, mandates, and the question of who bears the operational risk when an agent buys €500 worth of the wrong item.

American Express made an early move here, rolling out Agent Purchase Protection, an industry-first promise to cover eligible losses when a registered AI agent makes a mistake on its network. It’s a start, but more players need to step up and agree to cover risks for agentic commerce to scale.

In travel, as one panel put it, the agents do more than buy a product. They are fulfilling time-sensitive promises with multiple complexities and edge cases, which are harder to delegate than the purchase of a pair of sneakers.

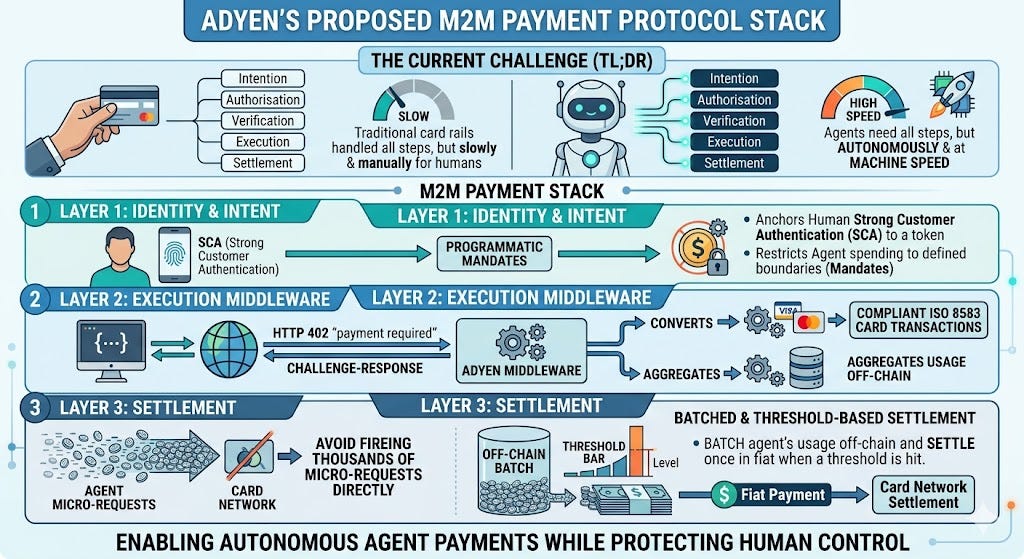

The topic closed for me with a technical session from Adyen on: The Foundations of Future Commerce: Building a Merchant-First Approach to Agentic Systems. In it, they showed that although agents already pay autonomously at machine speed, infrastructure problems still keep agentic payments stuck as science fiction. TL;DR: Card setups were built to handle intention, authorisation, verification, execution and settlement, just not all of it autonomously and at machine speed. Their proposed fix is an open protocol stack for machine-to-machine payments, in three layers.

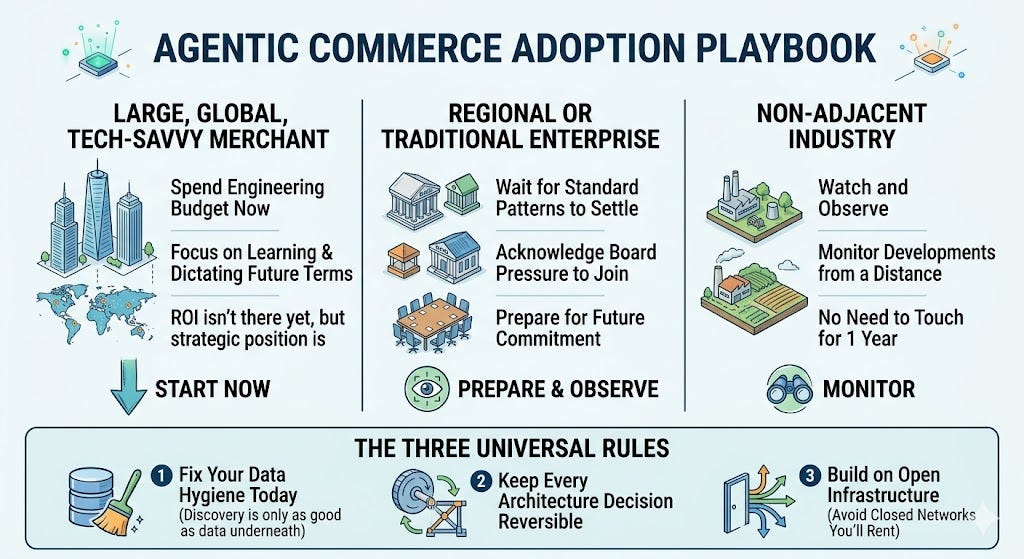

They closed by sharing a rough playbook on how to look at this topic by company size and avoid FOMO. 👇

Fraud, security and identity.

Behind every AI session, the big question was “Trust.”

In their session, NVIDIA and Snowflake pitched AI “learning the language of money” with examples of a foundation model being trained on the full transaction flow, which powered fraud risk and customer value simultaneously.

This compelling vision has a prerequisite of unified data. However, most fintechs and banks have it trapped in silos with different owners and zero interoperability.

Before any model can learn the language of money, somebody has to build the data pipeline that feeds it. In the agentic age, this means fraud prevention models and other AI models can’t be bolted on after the fact. They have to be in the core stack of the provider (merchant, fintech or bank) and be close enough to authenticate the buying agents and various third-party decision-making agents. You give AI all the context in fighting fraud or you don’t use it at all. You fight fraud with more informed AI.

No human, and no traditional ticket-by-ticket review, can validate the seven million microtransactions a second the optimists were throwing around on stage.

Identity presents the same problem. Watching the LSEG’s Identity Gateway in action showed where cross-border KYC and agent identity are heading. Once you have to prove who, or what, is transacting, especially when the “who” is increasingly a bot, you really only have two options. Either we make peace with registering our agents through some future “Know Your Bot” process, the way we onboard humans through KYC today. Or we hand agent verification and trusted-spend mandates to the handful of giants already treating agentic identity as a land grab (Stripe, Visa, Amex, Adyen, Amazon) and let them decide which agents are allowed to spend, and how much.

Sovereignty: Taking a Swing at the Card Duopoly, and the US Dollar

CBDCs are terrible, obviously, but politicians are wary of a certain man residing at Pennsylvania Avenue, and his continuous meddling with the global world order. Protecting digital sovereignty seems to now matter more than owning an additional $2T in US Treasuries, even if that is the best solution. — Excerpt from last year’s post

If I had a dollar for every time I heard “SEPA and A2A just work, why do we need this?” during this conference, I’d have eight dollars.

Tired of hearing it between demos, I started reminding people that Visa and Mastercard also began by solving American-specific problems before they scaled globally. If Europe wants to take sovereignty seriously, its decision-makers need to look past “SEPA and A2A just work.” That complacency is what keeps them blind to the global payments problems that a continental solution could greatly impact.

Enter the UK Payments Initiative.

Thirty-one banks and fintechs came together under UKPI to launch a commercial Variable Recurring Payments scheme. It’s the first shared rulebook, commercial framework, and operational standard for recurring account-to-account payments.

“Me-to-me” VRP, sweeping money between your own accounts, has existed for years. Commercial VRP unlocks the ability for businesses to collect variable recurring payments straight from a customer’s bank account, with consent and predefined limits. Subscriptions without cards. Utilities without Direct Debit. With the right political will and adoption, this is a credible alternative to Visa and Mastercard, and one that can scale globally.

There’s a planned Wave 2, where e-commerce and broad merchant adoption arrives. Merchants can offer discounts to move subscriptions off cards, kill card-on-file risk, and stop losing payments to expired cards.

This may be the closest the industry has come to a real answer on whether open banking can challenge the card duopoly.

For how it came together, there’s an 11:FS podcast taped on the floor with the CPO of Acquired, a launch partner.(here).

Multi-rail counter-attack.

“Efficiency in financial infrastructure is ultimately a matter of sovereignty, and the Euro’s role will depend on whether it rides the rails where global value moves,” said Sir Howard Davies, chairman of the supervisory board of Qivalis (the consortium of European banks building a euro stablecoin).

Even the ECB’s own efforts, from the digital euro to its warnings about dollar stablecoins, point towards European sovereignty and the protection of European capital markets.

UKPI, Wero and EPI are a sovereignty play as much as a pricing one. Beyond the press releases, the point these leaders are trying to make reads thus: Don’t let the dollar set monetary policy in Europe.

When you consider the point the co-CEO of Kraken made on stage about tokenization allowing anyone, anywhere to buy any asset, the ECB’s capital flight concerns—local European wealth being easily converted into a USD stablecoin to buy US government debt—no longer seem alarmist. Tokenized markets can now punish inflationary economies faster than ever, so every central banker should be alert to this and strive to protect their sovereignty and local capital markets.

Europe will have Qivalis, UKPI and Wero scaled up by year-end. Africa has no such answer. With the IMF warning that Nigeria’s surging use of dollar stablecoins—which account for 60% of sub-Saharan Africa’s stablecoin inflows—blunts monetary policy efforts, the creeping digital dollarisation is a concern. Bringing PAPSS on-chain and pushing compliant local-currency stablecoins like cNGN shouldn’t be an urgent roadmap item for Nigeria and the continent.

In summary, in a highly globalised and connected world, local currency stablecoins may have little to no utility, but their existence is important for preserving monetary policy and local capital markets. Every USDT/USDC held outside of America is a bet against the local economy in favour of US debt.

Traditional vs Programmable Money

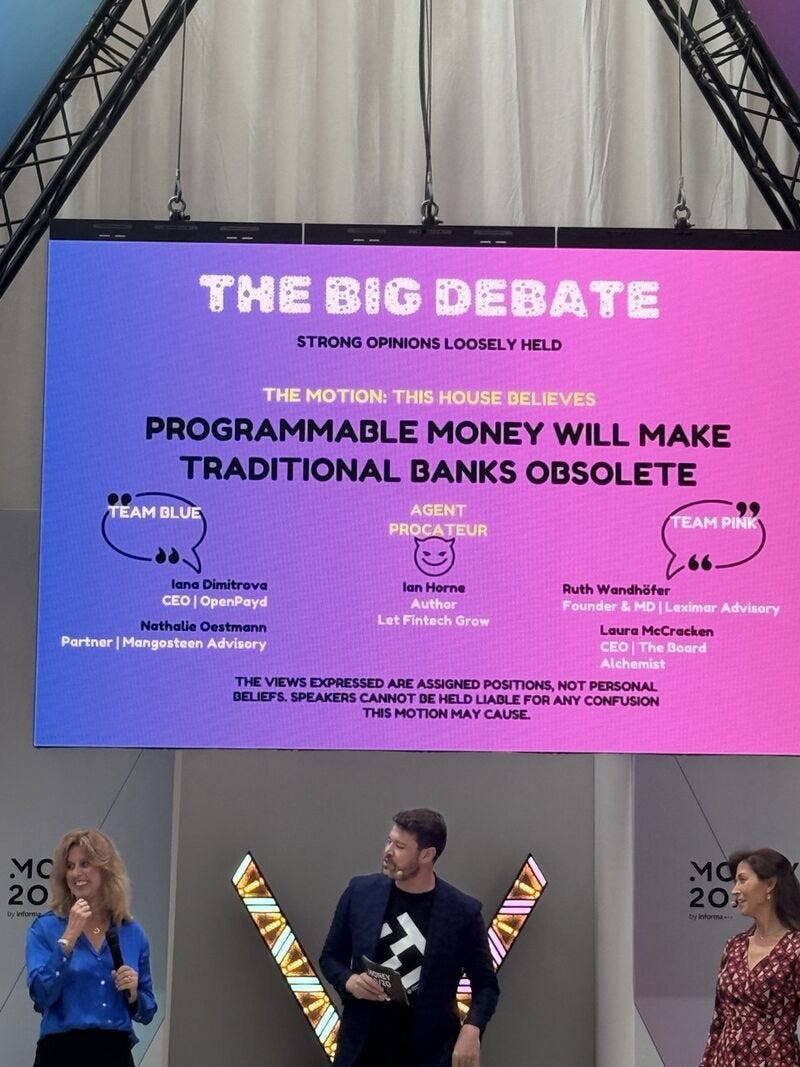

The best part of the show for me was the closing session, a “strong opinions, loosely held” debate on whether programmable money makes traditional banks obsolete. Chaired by Ian Horne, Author of Let Fintech Grow.

It created the right kind of tension and engagement and was a masterclass in politicking: with debaters saying just the right thing to get a rise out of the room. It played like an in-person performance of those ridiculous bank-vs-fintech/crypto fights on Twitter/X and LinkedIn, where everyone is selling snake oil.

A clear split is emerging. Traditional rails offer stability and the legacy comfort of compliant trust. Programmable rails are being rebuilt as tokenised, agent-native wrappers that settle money in seconds and hand custody back to the consumer.

Fighting ideological tribal wars feels good in the heat of battle, but the truth of the matter is that nobody cares about a specific stablecoin or a specific network. People just want the most efficient way to move money from A to B, and what they really don’t want is to become a captive tenant on yet another closed network.

The vast majority of financial services still run on traditional rails, and the next layer is being built on top of the old one rather than outside it. So these arguments would serve us better if we aimed at building an integrated financial system for speed, transparency, resilience and compliance instead of scoring ideological points.

How we get there is the crux of the book the Money 20/20 team, led by Scarlett Sieber, aptly launched on the Intersection Stage: The New Intersection of Money: Where TradFi and DeFi Converge

Final Show Thoughts

From the outside, this event looks like a snapshot of the overall financial services industry. I prefer to view it as a forward-looking lens of what the whole industry will look like twelve months from now.

At over 7,000 guests and a comparably smaller show than last year, the sheer number of European fintechs fighting to survive in the same market rather than expand was hard to miss. Most have built for one or two markets, while all are leaning on the same handful of infrastructure providers. Some consolidation has to happen to prevent an unfortunate event of creative destruction.

There are too many players selling infrastructure, and when customers keep buying their own infrastructure providers (Mastercard’s ~$1.8bn deal for BVNK being an example), the rest are left in a compromised position.

Getting bought is one exit; going public is the other (e.g OpenPayd). If the wager underneath all of this is that the next decade of finance won’t be defined by faster cards or cheaper wires but by “money that moves on its own” and “money moving at the speed of the internet”, then it is probably smart to start building up a stock-market narrative and the appetite to match this thesis.

So if last year I closed by asking for more agentic commerce use cases and real-world applications, this year I’ll predict consolidation and capital efficiency.

The boring questions of who actually pays for this, at what margin, across how many markets, and how to pay salaries all need to be answered.

America has too many fintechs exporting American solutions to the rest of the world; Europe has too many fintechs chasing the same single market; and Africa has too few that have scaled across one continent.

If the Western story for the next twelve months is creative destruction or consolidation thinning a crowded field, the African story is the opposite: the field is wide open, with the prize going to whoever can connect enough markets at scale.

If the future of finance is going to be agentic, it also has to be honest, to earn and deliver trust.

Till next time.

*The views expressed in this article are entirely my own and do not represent the views of my employer

A few nice links

#124 - Why Most “Next Big Things” in African Fintech Won’t Inflect - Frontier Fintech Newsletter

Hacks vs Artists - Nick Maggiulli

How stablecoins became part of Nigeria’s central bank’s plan for payments - Techcabal

Europe's fragmentation is a stablecoin opportunity - Jevgenijs Kazanins

Do consumers really want agentic commerce? - Payments Culture

ZelleUSD — A Private Coin - Noyes Payment Blog

Greenspan Left a Lasting Mark on America—and Me - The Wall Street Journal

Our Achilles Heel - Collaborative Fund

A busy year for Nigeria’s Central Bank - Crossover post on NotaDeepDive

The Nigerian Fintech Starting XI - Crossover post on NotaDeepDive