Global Cross-Border transactions. Will we ever get real time payments?

or why sending money from Nigeria to Ghana is hard

For over 25 years, Nigerians have benefited from the speed of payments offered by NIBSS (Nigeria Inter-Bank Settlement System), enjoying the convenience of instant local payments, leading many to assume this is how banking works globally. Across Africa, mobile money services are more popular than local banks in providing similar convenience, enabling near-instant transfers within borders.

However, as more Africans, particularly Millennials, engage with the global economy, they quickly discover that international payment systems do not offer the same real-time capabilities they’re accustomed to at home. Despite advances, sending and receiving money across borders remains slow and fragmented.

The major problem here is sending money quickly from a country A bank account to another country B bank account. For a successful instant transfer to meet the user’s needs, they must often use third-party mechanisms such as crypto, PayPal (where available) or offline money transfer agents connected to the local payment rails to settle this transaction.

Consider this scenario: I’m a Nigerian traveller visiting Kenya with a bank account in NGN or USD. I want to buy a SIM card at the airport or pay my cab driver in KES or USD. Unfortunately, my bank and the local bank have no interoperability in settling the transaction instantly. My quickest option is to download mPesa, complete KYC for a local mobile wallet, find an agent, visit an ATM, or use cryptocurrency—all of which introduce friction and do not scale globally due to varying payment systems and regulations.

Now that the problem has been explained in brief, and we propose a scalable solution (because PayPal and crypto are not scalable solutions), let us define the components of the problem today.

SWIFT: The Backbone of Global Financial Messaging

SWIFT (Society for Worldwide Interbank Financial Telecommunication) was created in 1973 to provide a standardised, secure global financial messaging service for banks worldwide. It offers a platform for banks to communicate using a common “system language” for various transaction types, including international payments, securities trading, treasury operations, trade finance, currency trading, and general communication.

Among these, trade finance and currency trading are the most common and high-volume activities, where both banks and SWIFT derive the most value and revenue.

Today, approximately 11,000 banks across 200+ countries are part of the SWIFT network, making it an effective system for banks to communicate and process transactions(estimated 50 million messages and $5 trillion processed daily). Similar to the Bloomberg terminal in trading, SWIFT is the predominant platform for global bank communication, handling the majority of transaction types and messaging categories.

The standard SWIFT settlement window for international transfers is 2-5 days, with processing fees charged by both banks according to their agreed fee structure with SWIFT. (For example, a $50 transfer from Nigeria to Canada could incur processing costs of $24.)

While this system may not be optimal for most low-value transactions – which has led to the rise of alternatives like cryptocurrencies, PayPal, and neobanks – it works for the high-value transactions that banks and customers moving large volumes internationally optimise for. As long as SWIFT continues to just work for this purpose, there exists little incentive to address the challenges associated with low-value transactions, neither should they be expected to.

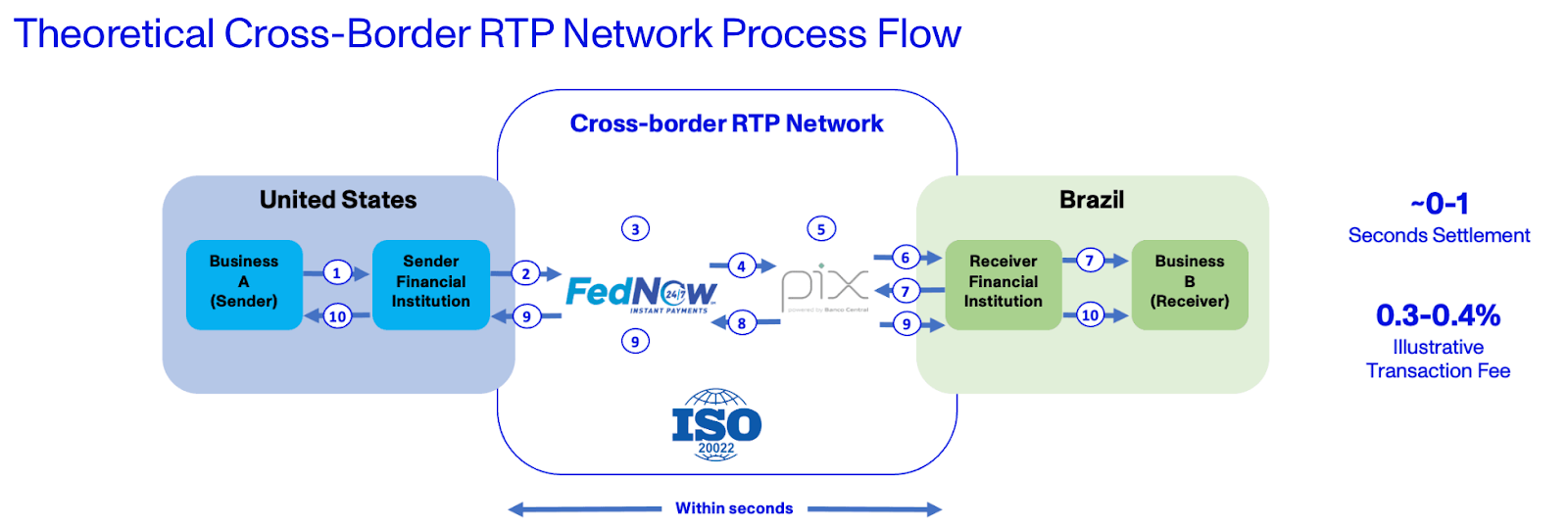

Note: Swift is currently experimenting with rolling out RTP for international transfers in 80 countries. Their current bottleneck is integrating with the various local and regional switches to make these transfers faster. – Honestly, that is cumbersome

KYC and AML/CFT Regimes

KYC (Know Your Customer) and AML/CFT (Anti-Money Laundering/Combating the Financing of Terrorism) policies are designed to restrict various forms of financial crime globally. While these policies – though imperfect, vary across jurisdictions, a basic level of KYC is expected from all users of financial services.

Our example traveller visiting Kenya shouldn’t need to complete onboarding processes for apps across 200 jurisdictions just to access local payment systems – such a requirement does not scale and is unrealistic.

AML thresholds differ worldwide, but one consistent policy is the $10,000 cap on cash transactions, requiring documentation for amounts exceeding this limit. Banks worldwide have adjusted this threshold based on their internal compliance policies, but the underlying principle remains: to reduce the volume and impact of illegal money flowing into the financial services space.

While current KYC and AML policies are imperfect, they serve as base-level safeguards for regulatory compliance and protection of the system from bad actors.

I hate having to go through KYC to send just $20, but this is currently unavoidable. These compliance checks inevitably increase transfer processing times.

Maybe in the future, an entity would get lucky and solve the problem of a globally compliant KYC solution covering 200+ countries. Such a solution would theoretically provide comfort for banks, regulators, and fintechs to serve citizens of sanctioned states and countries on the FATF (Financial Action Task Force) grey and black lists – a topic worthy of a separate article.

Lack of Interoperability between networks

The final point I want to share about the reason for this is the lack of interoperability of bank payment networks across the world. Open banking and central switches are relatively new concepts in banking and are very much localised. – Think NIBSS (Nigeria Inter-Bank Settlement System) in Nigeria, GhIPSS (Ghana Interbank Payment and Settlement Systems) in Ghana, NPCI (National Payments Corporation of India) in India, and SIBS (Sociedade Interbancária de Serviços) in Portugal. These systems have successfully connected banks within their respective countries and innovated in the area of real-time instant payments.

These solutions are however localised and the world in which the switches can interact seamlessly with each other does not exist yet, and may never exist due to sovereign risks. (this is why you can not send money instantly from GTBank Nigeria to GTBank Ghana despite their shared brand)

Given this problem, SWIFT remains the most available solution to banks for interoperability and communication standards. As Africans, we can only hope that the PAPSS (Pan-African Payment and Settlement System) network gives us an equivalent of SEPA, to allow our banks to communicate with each other across borders.

Note: During research for this post, the PAPSS website was down for an extended period. Goodluck.

Current Solutions

Some solutions exist in the market today for making real-time cross-border payments, but they have varying levels of complexity and caveats that prevent them from scaling as quickly as banks.

PayPal (and digital wallets in general)

This category of products is the most common alternative to solving this problem. Currently, with 400 million users globally, PayPal provides a way for most global travellers to send money instantly to people across the world.

The kicker though is that PayPal is not universally available (eg in Nigeria) and the intended receiver of the payment may not have a PayPal (or a global digital wallet) account. Additionally, as these entities are not banks, their KYC efforts across multiple jurisdictions are minimal, and they can close your account for any reason due to their limited abilities to conduct thorough checks.

Crypto – honestly no comment

Neo banks (Wise, Revolut, Monzo, Nubank, Starling,)

Digital banks are not banks, and they are not necessarily better than banks at traditional banking – Now that I’ve gotten my bias out of the way, let’s talk about the core issue.

As shared earlier in this post, banks have 11 unique cross-border use cases they deal with daily, and cross-border real-time payments may be their lowest value driver. This has allowed neo-banks and remittance companies to innovate around this problem by offering cheaper and faster ways of doing so *(often subsidised by VC money)*

For instance, Wise connects to various payment systems like the American ACH (Automated Clearing House), SWIFT, SEPA (Single Euro Payments Area), and numerous other switches to facilitate near real-time payments and transactions via the most appropriate channel for each destination. Traditional banks, in contrast, typically rely on regional switches or SWIFT to route transactions.

While this makes it easy and quick to process payments, the KYC problem exists again.

These accounts are not globally accessible, do not send money to all destinations in the world (Wise, for example, only recently resumed transfer services to Nigeria) and may still use SWIFT to send the transaction in 2-5 days.

And for my favourite Neo bank tidbit: Because they all mostly employ a lite version of global KYC and regulatory standards, customers are often subjected to sudden account closures without being properly informed of the rule they broke(if any).

Yes, that account you opened because you wanted to send $20 can be closed when you receive $5K and the bank would be right to do so. It’s not racism or discrimination, they just lack the capacity (human and financial) to investigate and tell you specifically what you have done wrong and why.

Money transfer companies

Before the advent of digital banks and the new age remittance companies, The OG money transfer companies such as Western Union, RIA, and Moneygram allowed immigrants across the world to send and receive money to and from their loved ones back home via their agents scattered all over the world. These were some of the most convenient and accessible forms of remittance and cross-border payments available in the market.

In the 2010s, these companies worked their relationships with their partner banks to create a service that allowed the receivers to receive the remittances in their bank accounts within minutes. In my opinion, this is the closest we’ve gotten to solving the cross-border payments challenge at scale.

Despite that, the problem of interoperability still exists here, as the service requires the sender and receiver’s banks to partner with the same money transfer company, as there is no current system that allows interaction between different providers—meaning MoneyGram transactions, for instance, can’t be routed through Western Union, and vice versa.

Scale /skeɪl/: (verb) Does the proposed solution apply to 200+ countries?

Possible Solution

A new kind of remittance platform?

Perhaps it's time to reconsider the current money transfer process. Money transfer companies have individual relationships with banks, enabling these banks to extract more complementary value - such that I can walk into a MoneyGram kiosk in India and within 30 minutes, my receiver opens their Ecobank Bank app in Kenya, Uganda or Ghana to receive the money in their account as simple as that.

How about going a step further on this existing remittance infrastructure the big players have and building an instant cross-border payment platform that solves this problem on the bank account layer, rather than creating a new layer that would be difficult to scale uniformly across 200 countries?

Step 2 in this scenario would be distribution and ensuring that the feature is available to virtually all the banks across all territories of the world, that way I can theoretically open my Deutsche Bank app in Germany, click the Western Union option and send money to someone to receive in their CBD Ghana account, within 45 seconds, instead of initiating a SWIFT transfer that takes three days.

The closest scalable solution we have at present (apart from PayPal) would be for all the world’s banks to connect to a "better, faster" version of SWIFT designed specifically for these “low-value” cross-border transactions.

The truth as I have shared earlier in this post, is that local banks can't solve this problem. We need to acknowledge that the banks can not solve this problem due to regulation, international law, foreign diplomacy, and third currency illiquidity constraints.

This is the only solution for this problem I can see at this point because, at the end of the day, it sucks having to KYC multiple times or waiting 5 days to receive $20. It is also unrealistic to expect global adoption of crypto stablecoin solutions due to various reasons from regulation, crypto complexity, literacy levels, bias, and even past negative experiences with crypto.

A few folks have suggested all local and regional switches connect with each other to solve this, but in this polarised and heated-up international political climate, the chances of that happening are slim to none.

Paypal is not accessible to up to 80% of the world, and most other common digital wallets, are local rather than international. The one accessible and scalable financial services product available to the entire world(4.5 billion people) today, is a traditional bank account, and as such, this problem can only be solved at the bank account layer.

Shout out to everyone who has innovated around the space but the current closed network solutions do not scale. Ultimately, $20-$5,000 transfers are not attractive enough for banks to earn from. International money transfer to them is just the byproduct of the larger pie that is currency trading.

And when you own a barrel of oil, you don't refine asphalt, when petrol and diesel are available.

Some posts take a village to complete to ensure accuracy and erase bias where necessary. Thanks to my Ogas Teju, Sam, Binjo, Neche, Busolami, MJ, and Lade for their reviews, comments and discussions on this topic.

References: